Table of contents

Homeownership remains a cornerstone of the American Dream. For veterans and military families, VA loans provide a unique opportunity to achieve this goal. VA loans, backed by the Department of Veterans Affairs, offer significant benefits compared to traditional mortgage options. In this guide, we’ll explore the ins and outs of VA loans and eligibility requirements. We’ll also show you how to navigate the process to secure a home for you and your family.

Understanding VA Loans

VA loans are mortgage loans specifically designed for eligible veterans, active-duty service members, and certain military spouses. The Department of Veterans Affairs guarantees a portion of the loan, which allows VA-approved lenders to offer more favorable terms to borrowers.

The VA loan program began in 1944 as part of the Servicemen’s Readjustment Act, also known as the GI Bill of Rights. Since then, they have helped millions of military families purchase homes or refinance their existing mortgages.

One crucial aspect of VA loans is the entitlement. Entitlement refers to the amount the VA guarantees for each eligible borrower. This guarantee reduces the risk for lenders. With reduced risk, lenders are able to provide loans without requiring a down payment or private mortgage insurance (PMI).

Advantages of VA Loans

VA loans offer several advantages over conventional mortgages:

- No Down Payment: Typically, no down payment is required, making homeownership more accessible for veterans and military families.

- No PMI: Unlike conventional loans, VA loans do not require borrowers to pay PMI, which can save hundreds of dollars per month.

- Competitive Interest Rates: Due to the VA guarantee, lenders can offer competitive interest rates, often lower than those of conventional loans.

- Lenient Credit Requirements: VA loans have more forgiving credit requirements, making it easier for borrowers with less-than-perfect credit to qualify.

- Limited Closing Costs: The VA restricts the amount borrowers can be charged for closing costs. This helps keep the home buying process more affordable.

These benefits can save borrowers a significant amount of money over the life of the loan. This makes VA loans an attractive option for those who qualify.

Eligibility Requirements

To be eligible for a VA loan, borrowers must meet specific service requirements. These requirements vary based on whether the borrower served on active duty, in the National Guard, or the Reserves, or is the surviving spouse of a service member.

Generally speaking, active-duty service members must have completed at least 90 continuous days of service during wartime. 181 continuous days of active duty service is required during peacetime. National Guard and Reserve members must have completed at least six years of service, or 90 days of active service during wartime.

Surviving spouses of service members who died in the line of duty or as a result of a service-connected disability may also be eligible for a VA loan. In some cases, remarriage may impact eligibility if the spouse remarried before the age of 57 or before December 16, 2003.

To apply for a VA loan, borrowers must obtain a Certificate of Eligibility (COE). The COE verifies borrowers’ eligibility based on their service history. We will typically require a copy of the borrower’s DD-214, which provides information about their military service, to obtain a COE.

VA Funding Fees

In most cases, the VA charges a funding fee to help cover the costs of the loan program. This fee is a percentage of the loan amount and varies based on the borrower’s service history, the type of loan, and whether it’s the borrower’s first-time using a VA loan. Some borrowers, such as those with service-connected disabilities or surviving spouses of service members who died in the line of duty, are exempt from the funding fee.

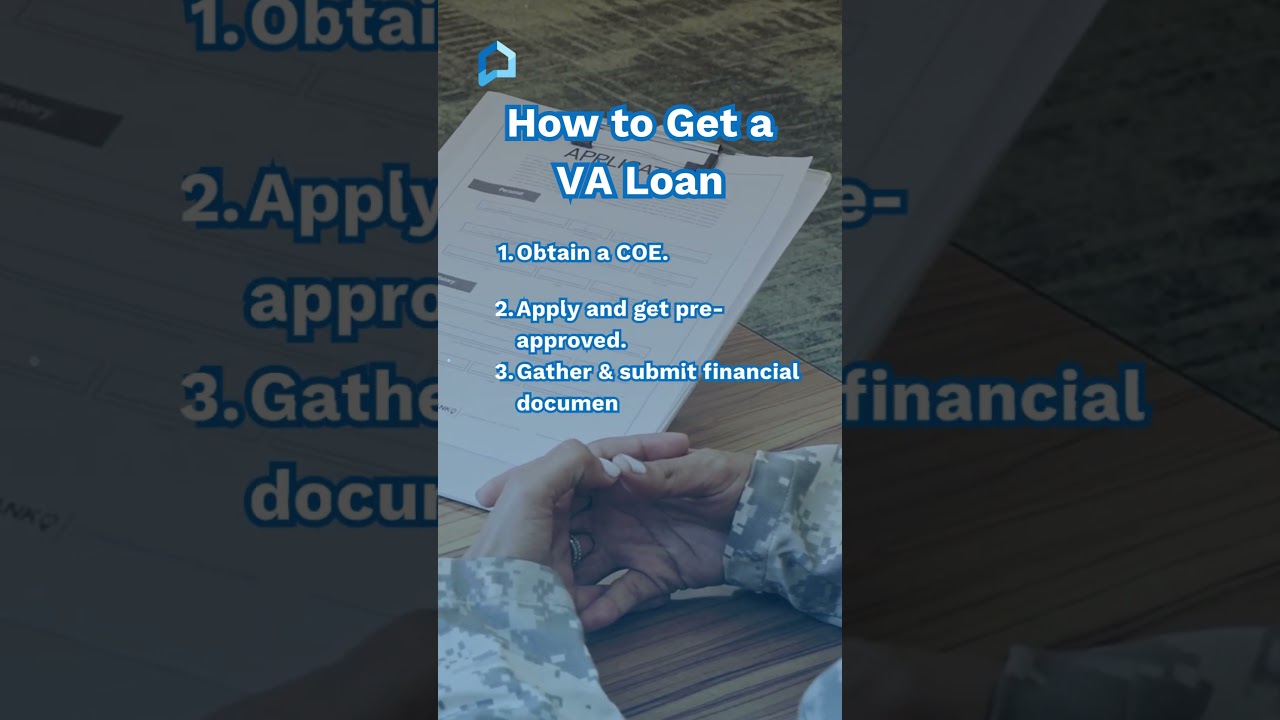

How to Apply for a VA Loan

Applying for a VA loan involves several steps:

- Obtain a COE.

You’ll need a COE to verify your eligibility. We can help you obtain this document using your DD-214 or other relevant service records.

- Get pre-approved.

Before you start house hunting, it’s a good idea to get pre-approved for a loan. This process involves filling out an online or over the phone loan application, and we’ll give you an estimate of how much you can borrow.

- Gather and Submit Documentation.

Once you have applied for a loan, you will need to submit supporting documentation such as pay stubs, tax returns, and bank statements.

- Get a home appraisal.

The VA requires a home appraisal to ensure the property meets its minimum property requirements (MPRs). An appraiser will evaluate the home’s condition, safety, and market value to ensure it’s a sound investment.

- Loan approval and closing

After the appraisal, an underwriter will review all documentation and decide whether to approve the loan. If approved, you’ll move on to the closing process, which involves signing paperwork and finalizing the loan terms.

VA Loan Refinancing Options

There are two primary refinancing options available: the Interest Rate Reduction Refinance Loan (IRRRL) and the VA Cash-Out Refinance.

- IRRRL: Also known as the VA Streamline Refinance, the IRRRL allows borrowers with an existing VA loan to refinance to a lower interest rate with minimal documentation and underwriting. This option is ideal for those looking to lower their monthly mortgage payment or shorten their loan term.

- VA Cash-Out Refinance: This option allows borrowers with a VA or non-VA loan to refinance and take cash out of their home’s equity. Borrowers can use these funds for various purposes, such as home improvements, debt consolidation, or other financial needs. The VA Cash-Out Refinance requires a full credit and income review, as well as a new home appraisal.

Tips for a Smooth VA Loan Process

To ensure a seamless process, follow these practical tips:

- Maintain good credit: Although VA loans have lenient credit requirements, it’s still essential to maintain a healthy credit score. Make sure to pay your bills on time, keep your credit card balances low, and avoid applying for new credit before seeking a mortgage.

- Manage your debt-to-income ratio: Lenders consider your debt-to-income (DTI) ratio when evaluating your loan application. Aim to keep your DTI below 41%, which is the maximum allowed in some cases.

- Work with a knowledgeable real estate agent: A real estate agent experienced in working with veterans and military families can help you navigate the home buying process. They will be able to address any VA-specific requirements or issues that may arise.

- Prepare for the home appraisal: Ensure the property you’re interested in meets the VA’s MPRs. Try to address any safety or structural issues before the appraisal.

Conclusion

VA loans offer significant benefits for veterans and military families, making homeownership more accessible and affordable. By understanding the eligibility requirements, advantages, and application process, you can make an informed decision about whether a VA loan is the right choice for you. Take advantage of this unique mortgage option and begin your journey towards homeownership with confidence and support.